簿記や会計の知識がまったくないと、少しわかりづらいと思いますが、チャレンジあるのみ!

会話

Amy: Good morning, everyone. Today, let’s discuss the fundamentals of accounting. Let’s start with the basics. Accounting is the process of recording, summarizing, and communicating financial information of a company. This allows us to track the financial position and performance of the company. Are you all ready to dive into the world of accounting?

皆さん、おはようございます。今日は会計の基礎について話しましょう。まずは基本から始めましょう。会計とは、企業の財務情報を記録し、集計し、伝達するプロセスです。これにより、企業の財務状況と業績を追跡することができます。皆さん、会計の世界に飛び込む準備はできていますか?

Ben: Yes, we are ready. Please go ahead.

はい、準備はできています。どうぞ、お願いします。

Amy: Alright, let’s get started! One key concept in accounting is the “double-entry system.” It is based on the principle that every financial transaction affects at least two accounts. Debits represent increases in assets or expenses, while credits represent increases in liabilities, equity, or revenues. This system ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced. Any questions so far?

それでは始めましょう!会計における重要な概念の一つは「複式簿記」です。これは、すべての財務取引が少なくとも2つの勘定科目に影響を与えるという原則に基づいています。借方(かりかた)は資産または費用の増加を表し、貸方(かしかた)は負債、純資産、または収益の増加を表します。このシステムにより、会計の等式(資産 = 負債 + 純資産)がバランスを保つことができます。これまでのところ、質問はありますか?

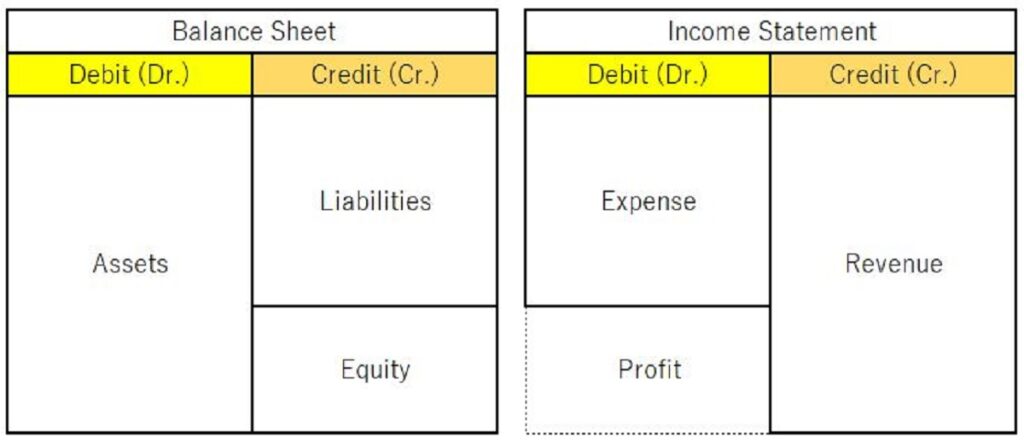

財政状態(資産がどれだけあって、その資産の裏づけとなる資金は借入などの負債からきているのか、または資本金などの自己資金がもとになっているのか)を示すのが貸借対照表(Balance Sheet)です。伝統的に、左側に資産、右側に負債・資本が表示されます。

Debit「借方」は左側、Credit「貸方」は右側にあたります。

一方、損益の状態を示すのが損益計算書(Income Statement、Profit and Loss Statement, P/L)です。借方に費用・損失、貸方に収益が記録されます。

Charles: I have a question. Could you give us an example of a specific transaction and how it would be recorded using the double-entry accounting?

質問があります。具体的な取引の例と、それを複式簿記会計のもとで、どのように記録するかを教えていただけますか?

Amy: Certainly. Let’s consider a scenario where a company uses cash to purchase office supplies. In this case, the office supplies account would increase and be recorded as a debit, while the cash account would decrease and be recorded as a credit. This transaction reflects the exchange of assets from cash to office supplies. By applying the double-entry system, we maintain the balance of the accounting equation.

もちろんです。例えば、企業が現金を使って事務用品を購入する場合を考えてみましょう。この場合、事務用品の勘定は増加し、借方に記録されます。一方、現金の勘定は減少し、貸方に記録されます。この取引は、現金から事務用品への資産の移動を反映しています。複式簿記システムを適用することで、会計の等式のバランスを保ちます。

Charles: I understand. So, all transactions require both debit and credit entries to maintain balance. How are revenues and expenses recorded then?

分かりました。ですので、すべての取引はバランスを保つために借方と貸方の両方の記入が必要なのですね。では、収益と費用はどのように記録されるのでしょうか?

Amy: That’s a good question. Revenues are recorded as credit entries. This is because they increase the company’s assets such as receivable or cash. Expenses, on the other hand, are recorded as debit entries. They decrease the company’s assets. By tracking revenues and expenses, we can assess the company’s profitability and financial performance.

いい質問です。収益は貸方の仕訳として記録されます。これは、収益が現金や売掛金など企業の資産を増加させるためです。一方、費用は借方の仕訳として記録されます。これにより、企業の資産が減少します。収益と費用を追跡することで、企業の収益性と財務パフォーマンスを評価することができます。

なお、英語で表現しても意味が適切に伝わっているか疑問の時は、「in other words」や「I meant that」として、別の表現で同じことを伝えると明確になります。

Denis: Thank you for the explanation, Amy. I have one more question. What about assets and liabilities? How are they recorded in the double-entry system?

エイミー、説明ありがとうございます。もう一つ質問があります。資産と負債はどのように複式簿記システムで記録されるのでしょうか?

Amy: Assets and liabilities are also recorded using the double-entry system. Increases in assets are recorded as debits, while increases in liabilities are recorded as credits. For example, if a company borrows money from a bank, the cash received would be recorded as a debit, representing an increase in the asset (cash), and the loan payable would be recorded as a credit, representing an increase in the liability (loan). This ensures that the accounting equation remains balanced.

資産と負債も複式簿記システムを使って記録されます。資産の増加は借方に記録され、負債の増加は貸方に記録されます。例えば、企業が銀行からお金を借りた場合、受け取った現金は借方に記録され、資産の増加として表示されます。一方、借入金負債は貸方に記録され、負債の増加として表示されます。これにより、会計の等式がバランスを保ちます。

Ben: I see. The double-entry system provides a structured way to record and track financial transactions while maintaining balance. Thank you for clarifying that.

分かりました。複式簿記システムは、バランスを保ちながら財務取引を記録し追跡するために一定の整理された方式を提供しているのですね。説明していただき、ありがとうございました。

「while maintaining balance」というように、while のあとに動詞の~ing形を用いて、「~するとともに、~しながら」という意味を表す用法があります。

Amy: You’re welcome! The double-entry system is the foundation of accounting, and understanding it is essential for accurate financial reporting. If you have any more questions, feel free to ask.

どういたしまして!複式簿記システムは会計の基礎であり、正確な財務報告のためには理解することが不可欠です。もし他に質問があれば、どうぞお気軽にお聞きください。

関連する用語

- Accounting (会計)

- Assets (資産)

- Liabilities (負債)

- Equity (資本)

- Revenue (収益)

- Expenses (費用)

- Balance Sheet (貸借対照表)

- Income Statement (損益計算書) Profit and loss statement や P/L ともいう。

- Cash Flow Statement (キャッシュフロー計算書)

- General Ledger (総勘定元帳)

- Trial Balance (試算表)

- Journal Entry (仕訳)

- Debit (借方)

- Credit (貸方)

- Accrual Accounting (発生主義会計)

- Cash Accounting (現金主義会計)

- Depreciation (減価償却)

- Amortization (償却)

- Chart of Accounts (勘定科目一覧表)

- Double-Entry Bookkeeping (複式簿記)

- Fixed Assets (固定資産)

- Current Assets (流動資産)

- Current Liabilities (流動負債)

- Long-Term Liabilities (長期負債)

- Inventory (在庫、棚卸資産)

- Accounts Payable (買掛金)

- Accounts Receivable (売掛金)

- Net Income (純利益)

- Gross Profit (粗利益)

- Cost of Goods Sold (COGS) (売上原価)

- Return on Investment (ROI) (投資利益率)

- Operating Income (営業利益)

- Operating Expenses (営業費用)

- Gross Margin (粗利益率)

- Net Profit Margin (純利益率)

- Earnings Before Interest and Taxes (EBIT) (利息・税引前利益)

- Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) (利息・税引・減価償却前利益)

- Return on Assets (ROA) (総資産利益率)

- Return on Equity (ROE) (自己資本利益率)

- Accrual basis (発生主義)

- Cash basis (現金主義)

- Contra Account (反対勘定科目)

- Prepaid Expenses (前払費用)

- Accrued Expenses (未払費用)

- Bad Debt (不良債権)

- Reserves (積立金)

- Contingent Liability (潜在的な負債)

- FIFO (First-In, First-Out) (先入れ先出し法)

- LIFO (Last-In, First-Out) (後入れ先出し法)