かつての会計は、P/L(損益)が重視されていましたが、

現在では、Balance sheetの重要性が再認識されています。

実務的には、P/Lが正しくても、B/Sが間違っていれば、

結果として、将来のP/Lに影響を与える点に注意する必要があります。

音声をどうぞ!

何度も聴いて、リスニング力をつけましょう。

同時に、発声するようにして、スピーキング力をあげましょう。

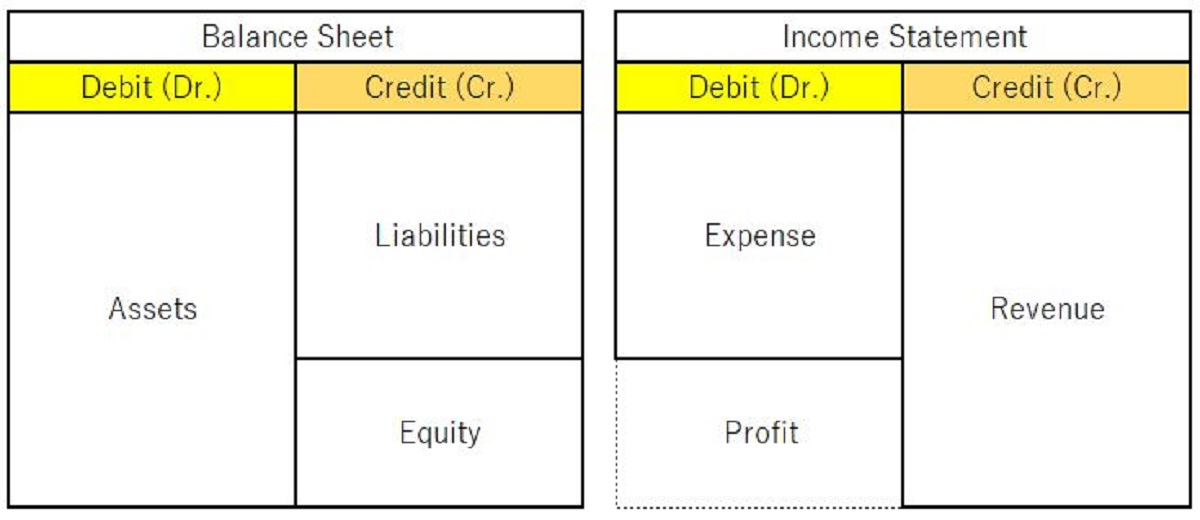

Introduction to the Balance Sheet(イントロダクション)

- The Balance Sheet, also known as the Statement of Financial Position, provides a snapshot of a company’s financial position at a specific point in time. It is one of the three main financial statements.

- 貸借対照表は、財務状態計算書とも呼ばれ、特定の時点での企業の財務状況のスナップショットを提供します。これは3つの主要な財務諸表の1つです。

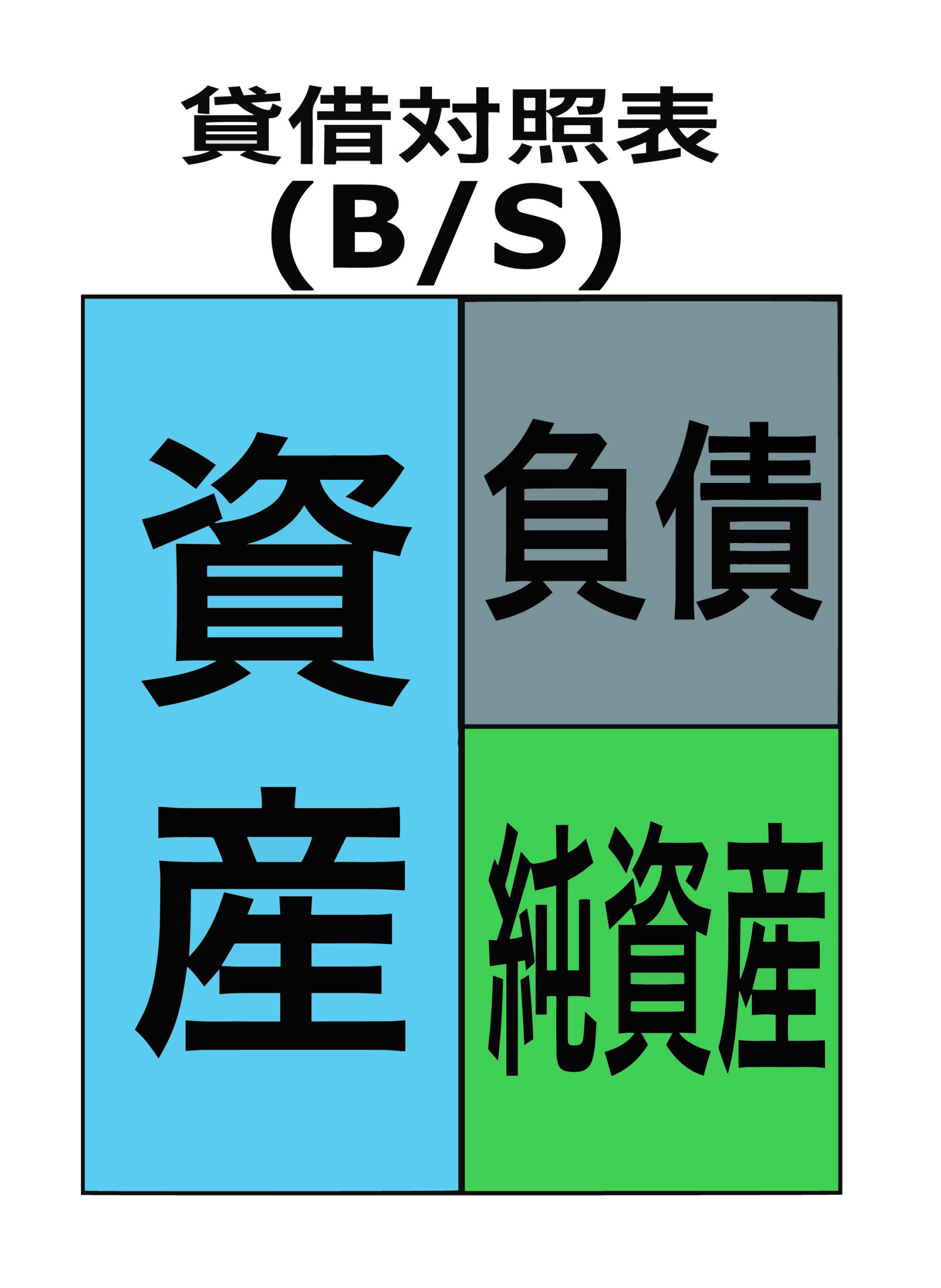

Structure of the Balance Sheet(貸借対照表の構成)

- The Balance Sheet is divided into two main sections: Assets and Liabilities + Equity. Assets represent what the company owns, while liabilities and equity represent what the company owes and the residual interest of the owners.

- 貸借対照表は主に資産と負債+資本の2つのセクションに分かれています。資産は企業の所有物を表し、負債と資本は企業が借りているものとオーナーの残りの利益を表します。

Assets Section(資産の部)

- Current Assets: These are assets expected to be converted into cash or used up within one year. Examples include cash, accounts receivable, and inventory.

- 流動資産: これは1年以内に現金に換算されるか、使い切られると予想される資産です。例には現金、売掛金、棚卸資産があります。

- Non-Current Assets: These are assets expected to provide value for more than one year. Examples include property, plant, equipment, and intangible assets like patents.

- 固定資産: これは1年以上にわたって価値を提供すると予想される資産です。例には不動産、プラント、機器、特許などの無形資産があります。

Liabilities + Equity Section(負債および資本)

- Current Liabilities: Obligations expected to be settled within one year, such as accounts payable and short-term debt.

- 流動負債: 1年以内に償還されると予想される債務、例えば買掛金、短期借入金などが含まれます。

- Non-Current Liabilities: Long-term obligations, such as long-term debt and deferred tax liabilities.

- 固定負債: 長期の債務、例えば長期の借入金や繰延税金負債などが含まれます。

- Equity: The residual interest in the assets of the entity after deducting liabilities. It includes common stock, retained earnings, and additional paid-in capital.

- 資本: 総資産から負債を差し引いた事業体の純資産に対する持分。資本金、剰余金、追加出資金などが含まれます。

Example of a Balance Sheet(実例)

- Let’s consider a hypothetical company’s balance sheet. On the asset side, it might have $50,000 in cash, $100,000 in accounts receivable, $200,000 in inventory, and $300,000 in property. On the liability side, it may have $150,000 in accounts payable and $100,000 in long-term debt. The equity section includes common stock of $50,000 and retained earnings of $350,000.

- 仮説の企業の貸借対照表を考えてみましょう。資産側では、現金$50,000、売掛金$100,000、棚卸資産$200,000、不動産$300,000などがあるかもしれません。負債側では、買掛金$150,000、長期債務$100,000などがあります。資本部門には普通株による資本金$50,000と剰余金$350,000が含まれています。

Analyzing a Balance Sheet(貸借対照表の分析)

- Investors and analysts use balance sheets to assess a company’s financial health. Key ratios like the current ratio (current assets divided by current liabilities) provide insights into a company’s liquidity.

- 投資家やアナリストは、貸借対照表を使用して企業の財務健全性を評価します。流動比率(流動資産を流動負債で割ったものなど)などの主要な比率は、企業の流動性に対する洞察を提供します。

Limitations and Challenges(制約と課題)

- While balance sheets provide a comprehensive view of a company’s financial position, they have limitations. For instance, the values are based on historical costs and certain assets may not be accurately reflected.

- 貸借対照表は企業の財務状況を包括的に示していますが、制約もあります。たとえば、値は歴史的原価に基づいており、一部の資産は正確に反映されていない可能性があります。

Understanding the balance sheet(まとめ)

Understanding the balance sheet is crucial for anyone involved in financial analysis, as it provides a comprehensive overview of a company’s financial position and helps stakeholders make informed decisions.

貸借対照表を理解することは、財務分析に関与するすべての人にとって重要です。なぜなら、それは企業の財務状況の包括的な概要を提供し、関係者が情報をもとにした意思決定を行うのに役立つからです。